How can FI best manage

the self-directed

banking channel?

Published April 5, 2022

Self-directed banking is key to the future for the banking industry as consumers becoming increasingly comfortable with using self-service technologies and their use of tellers shifts from everyday transactions to more valuable, consultancy-led conversations.

But as the self-directed channel increases in importance to consumers, for the financial institution (FI) it’s complex and time consuming to manage with security, compliance and availability (to name but a few) requiring intense and ongoing focus.

Running ATM networks today

When we look at the design of many ATM networks today, they were built decades ago with a single, very specific objective in mind: to dispense cash. But so much has changed and today consumers can complete as much as 95% of everyday transactions at the ATM – from cash and check deposits, bill payments, transfers, account opening and more.

As the functionality and variety of ATMs on the market increased, FIs expanded their ATM fleets, choosing the technology that best fit the business need – whether it was an ITM providing remote teller support in a grocery store, or in-branch cash recyclers or a cash dispense ATM at a train station. This led to FIs having fleets with ATMs from different vendors, operating different software which presented challenges in consistency in customer experience, functionality, security and compliance.

The introduction of the XFS standard, which provides the architecture for financial applications on Microsoft Windows Platforms, allowed FIs to benefit from interoperability across a variety of hardware endpoints, giving FIs greater freedom to choose the best-fit technology for their business while running a consistent software and user interface across all different models of ATM.

Today, the vast majority of – perhaps even all – ATMs support the XFS standard and all the leading ATM and ATM software vendors provide XFS compliant software that can run on multiple vendors’ ATMs. So, this has led to a many FIs running multivendor strategies to manage their ATMs – with multiple vendor ATMs running a single vendor’s software so they can have that consistent UI and customer experience whatever ATM a customer uses.

Multivendor strategies gave FIs much more flexibility. As a result, the last decade has seen a progressive migration towards multivendor strategies and today anywhere between 44% and 75% of ATMs are multivendor.

But a multivendor approach has drawbacks and as FIs look to innovate quickly and be more agile as new technologies go from fledgling to widespread adoption faster than ever before such a management model could be holding you back.

While the XFS standard is designed to make all software work together, there is an element of uncertainty in any implementation. Parts of the standard are open to interpretation and so there are always niggles and technical glitches when bringing different technology together which means it can take some resource to get the technology working as it should. Getting all elements of the software to work equally across all machines isn’t always as easy as plug and play.

Security will also be a concern. With data and services becoming increasingly mobile, the risks of breaches – accidental or through malicious actions – are rising. Working with third parties can potentially expose financial institutions to cyber risks which are out of their control. A weakness in the third party’s security infrastructure can put the systems of any business which works with it in danger.

Taking ATM management to the future

Today, many FIs view their ATM endpoints as a key part of their digital transformation strategies, offering exceptional digital first transactions that are seamless across the mobile and ATM channels.

In a connected age of open banking, cryptocurrencies and mobile banking, the current multivendor ATM network is increasingly limiting an FI’s ability to innovate and respond to changing market forces.

This opens up the option of employing an ATM as a service model. This allows financial institutions to outsource part, or the whole, of their ATM operations to third party providers. Experts can take on all aspects of ATM operations including distribution, installation, maintenance and cash management. This takes the burden off financial institutions, allowing staff to concentrate on further innovation and saving money in operating expenses.

- Efficiency: Iit’s easy to deploy with one software point of contact across the entire network in a seamless and integrated manner.

- Connectability: Ensuring consistent and reliable connectivity to the banking infrastructure which becomes much easier with just one system to configure.

- Security and compliance: Single handling of security and compliance across the whole network.

- Simplicity and consistency: If you’re having to interact with many different vendors, you can have a single and unified experience at all ATMs.

These benefits can be considerable. According to one study, in-house ATM operations can account for up to 35% of a FIs operating costs. With a single strategic partner, they oversee all operations including managing all the vendors being supported through the system.

What you get out of this is a more flexible, sophisticated and interactive solution in which ATMs are becoming FIs in a box. The vast majority of teller transactions are possible at the ATM including cash deposit, coin dispensing, account services, replacement cards and much more. Interactive teller services provide options such as face to face support through audio or video chat. FIs will be able to transform the traditional branch model, extending office hours and finding new ways to blend the self-directed banking experience.

All this new functionality, though, needs new and more advanced infrastructure to underpin it. Here at NCR, we’ve been working on upgrading software to provide enhanced functionality. We are, for example, the first to achieve ATMIA Next Gen Level 2 API certification with our Activate Enterprise NextGen ATM application. This allows for interoperability between vendors and provides access to banking and financial services which dramatically expand the functionality of the ATM. We are proud to be the first technology provider to achieve this milestone and empower modern applications delivering mobile like services through ATMs.

This is where the technology is going at the moment. What is advanced and innovative today will become commonplace tomorrow. The more technology customers are given, the more they expect which raises the bar for everyone.

This is the future and FIs will benefit by changing the fundamental business case around how they manage their ATM fleet. But they need to ask some probing questions: Are ATMs strategic to your branch strategy? Are you seeking to implement digital first engagements and journeys? Are you looking for vendors or partners?

Importantly, now ATM operators have options in regards to the operating models for their ATM network. Cloud and hosted solutions help reduce infrastructure costs, managed service options allow you to outsource more operations, while subscription pricing models provide more flexibility on the commercial costs to operate ATMs.

Digital innovation can always be a cause of anxiety – especially in the financial sector where every new advance creates a new avenue of attack. However, as long as FIs can understand the technology they work with and ensure all implementations are managed in the right way, they can open up all sorts of opportunities. And with ATM as a Service models growing in precedence, FIs don’t need to understand and manage the technology – they can outsource it to a partner who can take care of it all.

But the rewards are the same - aside from saving time and money, they can give the sector access to the benefits of open banking and all the growth potential which comes with it.

Success factor: A flexible, adoptable journey taxonomy

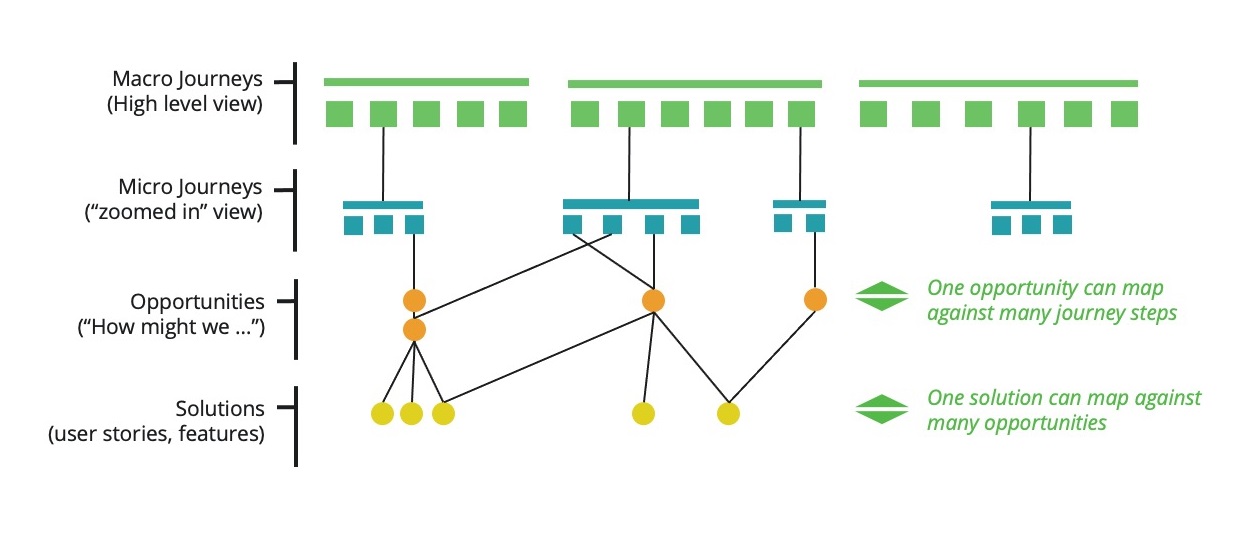

The key to managing journeys at the scale needed by an FI is establishing a clear journey taxonomy, and an effective platform to manage the journeys in one place. Executives and strategists may just be interested in a high-level journey – the macro journey, while product managers and designers may need to dive deeper into more granular steps of the journey – the micro journey. In design and strategy sessions, the team documents insights and ideas that will drive change over time – the opportunities. These are further broken down into individual units of work to make that change happen – the solutions.

The key differentiator from traditional journey mapping is a many-to-many thinking in the hierarchy, one solution to solve for multiple steps in multiple journeys. For example, a cash withdrawal journey for an ATM can be adapted as an ITM journey with minor variations. Doing this drives consistency in the experience and provides cohesion between the different customer experiences a FI offers.

In Summary

Implementing an effective journey management framework allows FIs to be close to the customer, create differentiating experiences in a rapidly transforming marketplace and even allows for better co-creation with partner organizations. The approach is quickly becoming best practice in the enterprise and the SMB space alike. The results back it up. Organizations that practice journey management are 1.6x more likely to outperform their peers1. Implementing robust journey management empowers FIs to be more agile and customer-centric across their entire portfolio.